A wealthy family may create a family office to achieve a wide range of objectives. These objectives may include realizing the benefits of pooled capital in order to maximize the universe of available investment opportunities at optimal cost; maximizing investment returns; ensuring financial security for future generations; and providing coordinated administrative, managerial and wealth advisory services. Regardless of the family’s objectives, certain legal and tax considerations often drive the structure and administration of a family office. The purpose of this Advisory is to provide an overview of the typical legal structure of a family office and the circumstances in which expenses incurred by the office may be deductible for federal income tax purposes.

LEGAL STRUCTURE OF A FAMILY OFFICE

A key consideration when setting up a family office is to select the structure that best suits the family’s objectives. There are several possible structures that may be considered, including forming a single-family office, joining a multifamily office, and/or incorporating a private trust company into a family office structure.

A private trust company generally provides fiduciary services to a single family and may be regulated or unregulated depending on the state of formation. If a private trust company is being considered, the family will want to select a favorable jurisdiction in which to form the company. For example, South Dakota, Nevada and Wyoming and several other states provide advantageous legal, financial and administrative rules for private trust companies.

Then there is the highly important and sometimes highly technical question of whether to establish the office as a C corporation, S corporation, limited partnership, limited liability company or some other legal entity. Limited partnerships, limited liability companies and S corporations generally are the entities of choice because they permit the flow-through of income and expenses to owners. In addition, a limited partnership or limited liability company is generally preferred over an S corporation because the limited partnership or limited liability company can have multiple classes of interests, including, for example, an incentive payment or “carried interest” that may be held by junior generation family members, while senior generation members hold preferred interests having a frozen value. Neither preferential distributions nor multiple classes of units are permitted for an S corporation. In comparison, advantages of a C corporation include, for instance, that income and expenses do not flow-through to the owners and, therefore, owners can avoid having to pay tax on phantom income. However, owners of a C corporation do not directly receive the benefit of preferential capital gains rates on their investments (i.e., all distributable income is taxed as ordinary income). The most common structures we see used are limited partnerships and limited liability companies. These are further described on the following pages.

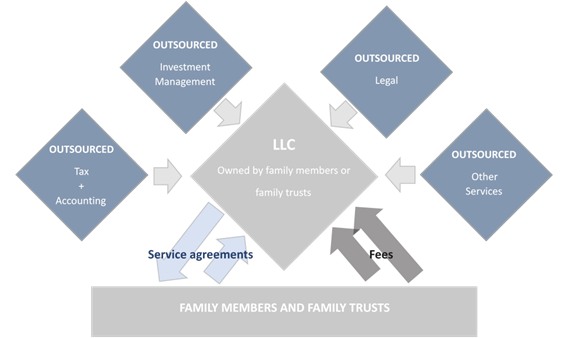

Family Office Basic Structure: Limited Liability Company

The LLC engages outside providers. Family members pay fees for those services.

| Structure | Tax Implications |

|---|---|

| Family office – Usually an LLC, taxed as a flow-thru entity, that provides services to family members. – Engages various outside providers for investment management, tax, legal and other services for a fee. – Family members (including trusts and other entities) enter into Client Service Agreements with the family – office to receive services for a fee. – Each household pays depending either on usage of services or pro rata | Prior to the 2017 Tax Act, there were three limitations on the deductibility of family office expenses, including investment management fees: 1. Together with other miscellaneous expenses, only amounts in excess of 2% of the owner’s AGI were deductible. 2. Pease limitation reduced itemized deductions by lesser of (i) 3% of adjusted gross income above certain thresholds, or (ii) 80% of all itemized deductions. 3. AMT taxpayers lost benefit of most itemized deductions. Now, per 2017 Tax Act, all expenses incurred “for the production of income” under I.R.C. §212 are not deductible through 2025. |

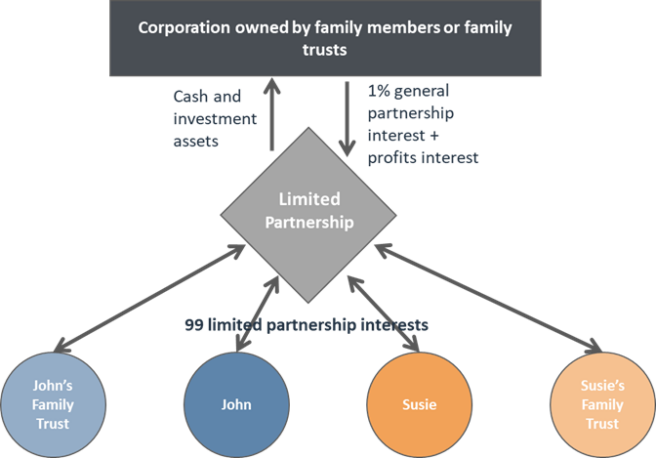

More Complex but Tax-efficient: Family Limited Partnership

The family office is a corporate entity and general partner; family members or trusts are limited partners.

| Structure | Tax Implications |

|---|---|

| – LLC or corporation, taxed as S or C corporation, to act as family office. – Family office acts as general partner of investment partnership. – Must be engaged in a “trade or business” to claim I.R.C. §162 deduction for family office expenses, including investment management fees (i.e., have goal of generating a profit on investment activities). – Provides services to family members (including trusts and other entities). – Has income from two sources: 1. Management services agreements – agreed upon fees for providing management and administrative services to family members and trusts (e.g. 1% of total assets value). 2. Profits interest (e.g. 20% of profits earned). | Family office is able to deduct expenses for: – Investment management. – Personnel/Payroll. – Office administration. |

Finally, depending on the type of investments, it may be advantageous to organize multiple business entities to hold the various assets managed by the family office. In a typical structure, separate entities would be created for various classes of investments made by the office. For example, the office may operate an “Alternative Investments Pool LLC,” a “Large Cap Equities Pool LLC,” a “Real Estate Investments LLC,” etc. Each limited partner or limited liability company member can decide which investment entities to participate in and how much to invest, while the family office would manage these investments and exist to house the administrative and operational functions of the office.

DEDUCTIBILITY OF ADMINISTRATIVE EXPENSES

A key objective that many families hope to achieve in forming a family office is the possibility of deducting certain administrative expenses relating to the business. A single member limited liability company is the simplest family office structure, however, the 2017 Tax Act suspended through 2025 the deductibility of many family office expenses, including investment management fees, for individuals, trusts and certain entities functioning only as an investment conduit for their individual owners. As a result, only family office structures that are actively involved in a “trade or business” can deduct certain family office expenses under current law. For example, a family office may be integral to the operations of a family business or the office itself may engage is such a high volume of trading activity, or receive most of its compensation through a profits interest, that the office itself constitutes an active business. This creates the potential for more favorable treatment of certain expenses (e.g., start-up costs, equipment and supplies, overhead and employee salaries). In these cases, such expenses may be above-the-line deductions, resulting in potential tax savings for the family office.

CONCLUSIONS

Individuals who are considering forming a family office or who have legal questions regarding family offices should consult experienced counsel. The Family Office and Strategic Investments practice group at Wiggin and Dana has experience with a wide variety of legal matters relevant to family offices, including tax and estate planning, tax compliance, governance, securities law, employment, real estate and other matters, and can assist individuals in forming and maintaining a family office that is specifically tailored to their short-term needs and long-term goals.

*****************************************************************************************************************

U.S. Treasury Circular 230 Notice: Any U.S. federal tax advice included in this memorandum is not intended or written to be used, and cannot be used, for the purpose of avoiding U.S. federal tax penalties. *****************************************************************************************************************